Upturn in ratings looks set to begin

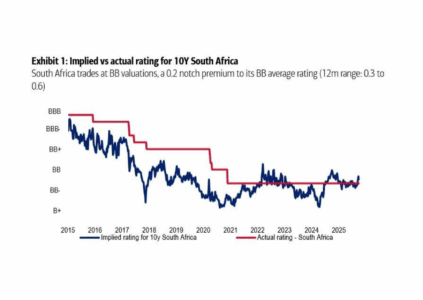

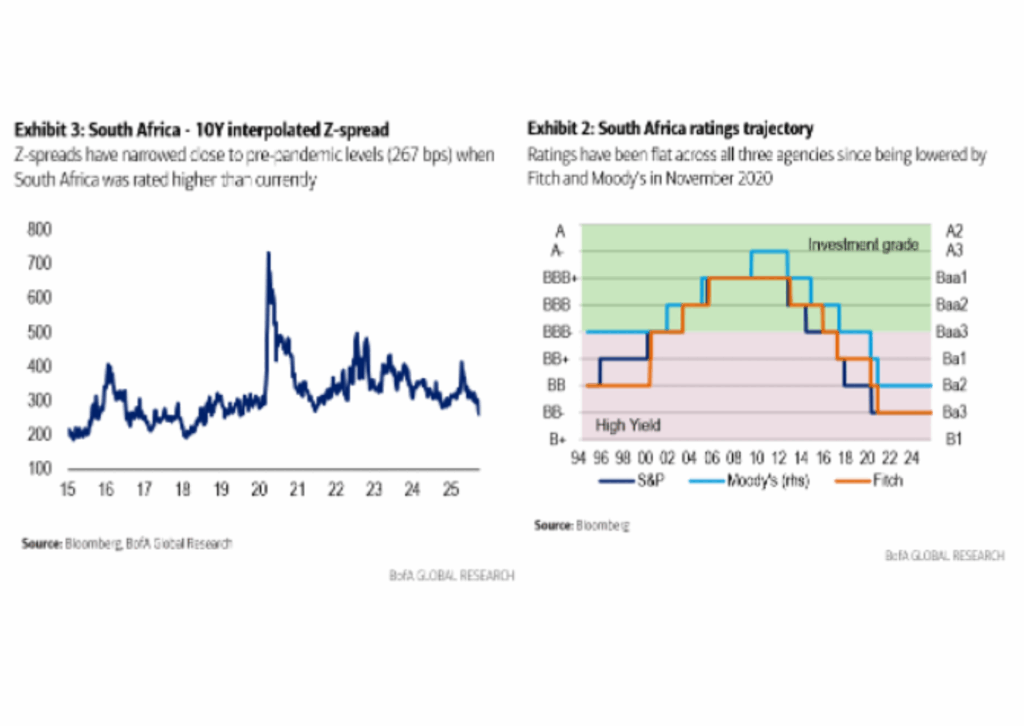

SA’s sovereign ratings have been unchanged for five years: Fitch BB-/stable; Moody’s Ba2/stable; S&P BB-/positive. However, near-term fiscal improvements could herald the start of an upward trend in the ratings trajectory. Delivering higher GDP growth could provide more upgrades. It’s not yet good enough for talk of investment grade, though.

Fiscal improvements to give the green light?

This fiscal year, SA could post its lowest main budget fiscal deficit since 2016. We see it at -4.1% of GDP, much better than the Budget baseline of -4.6%. The country has a firm grip on expenditure, and the pace of revenue collection is high, suggesting fiscal improvements. The Mid-Term Budget on November 12 should confirm this.

In addition, the fiscal outlook is even more positive from 2026, once Eskom financing is largely completed and headline deficits of <4% of GDP support large primary surpluses that should put debt to GDP back on a downward trend.

Higher GDP growth later could lead to more notches

GDP growth has disappointed in 2025 around 1%, but we think a catch-up is likely medium-term. Economic reforms are encouraging, and financial markets appear to view SA favourably. Bond yields are lower and CDS spreads are at tightest levels since pre-pandemic, responding to an improving Eskom, Transnet private participation, SARB’s move to a 3% target and likely fiscal improvements. And all this despite GNU (Government of National Unity) wobbles in 1H 25.

Fitch done for 2025, waiting on Moody’s + S&P

Fitch has already completed its 2025 reviews and will next meet in 2026. However, Moody’s (5 December) and S&P (14 November) will issue reports before year-end. They could find enough support to consider upward adjustments.

Will S&P move up or choose to wait?

S&P pulled back from an upgrade on 8 March 2023, after it had assigned a positive outlook a few months earlier. The pullback was driven by a 4Q 2022 GDP contraction that poured cold water on the positive economic outlook. 2023 was then dominated by record power cuts. Most recently, S&P moved to a positive outlook on 15 November 2024.

Usually outlooks for non-investment grade can be resolved within a year. There is room to wait if there are good reasons to convert that positive outlook to an upgrade. In our view, higher GDP growth is not yet one of those reasons, but likely fiscal improvements could nudge them toward an upward move.

S&P is likely to be the first mover upwards

In our baseline, we expect S&P to be the first mover: the next review is scheduled for November 14, or they could choose to wait another six months. Other rating agencies could follow suit from 2026. While 2025 GDP growth has disappointed versus 2024 expectations, the path is still up. We expect South Africa to grow at 1.2% this year, improving to 1.4% in 2026 and likely over 1.5% from 2027. Near-term GDP growth improvements are benefiting mainly from an increase in consumption. Our medium-term forecasts are still conservative – we need to see an investment uptick to be more bullish.

Energy shortages have been reduced with fewer power cuts, while logistics bottlenecks and other reforms are a work in progress. Economic growth forecasts are looking up. Transnet is moving ahead with private participation on the rail and ports network, while Eskom has turned a profit for the first time in eight years.

A first notch upgrade is possible should fiscal deficits decline sub-4% and debt to GDP decline, as the Treasury forecasts. That could set a firm trend over the medium term.

Fiscal improvements in MTBPS provide hope

Compared to a year ago, we are more positive going into the mid-term budget presentation. This is despite political brinksmanship when lawmakers could not agree on a budget framework between Feb and May 2025. Fiscal year to date (April-Aug), expenditures are only 4% higher. Spending is up 4% in the first five months compared to 4.3% in the same period in 2024. Debt service costs have increased by 4.5% compared to 8% at the same time last year. Overall, April to August 2025, revenue collections increased by 11% year on year compared to 3.6% at the same time last year. Specifically, corporate tax payments are up 7%, while Personal income taxes are up 8%, with VAT 11% higher. The recent surge since May in platinum group metals international prices could show in higher revenues for the December tax take.

Issuance reduction likely

Overall, the main budget deficit could undershoot the original target by as much as R50 billion. That would mean a budget deficit close to R310 billion versus the initial target of R360 billion and create room to reduce issuance. Then there is an additional discussion about whether the Treasury could access GFECRA (Gold and Foreign Exchange

Contingency Reserve Account) funds. Latest SARB assets and liabilities show a balance of R354.8 billion as of August 2025. The minimum buffer is R250 billion and it can be adjusted upward. In our view, a GFECRA drawdown of R30-50 billion could be utilised for issuance reduction in the 2026 budget.

GNU calm after a turbulent 1H 25

The May 2024 elections produced a government of national unity. The April 2025 GNU breakdown scare seems to have been solved as tensions have calmed. The GNU is likely to continue to hold, with inflection points being local government elections in 2026 and the ANC’s (African National Congress) elective conference in December 2027.

Methodology issues – light work to get one-notch upgrade

All rating methodologies pull down South Africa’s rating by at least one notch because of weakness in economic or public finances. Fitch’s indicative rating is BB+, then the rating committee adjusts it downward twice – for weak growth prospects relative to peers and for weak public finances given uncertainty about whether it can stabilise debt plus weak SOEs (state-owned enterprises). Moody’s indicative rating puts SA at Ba1-Ba3, while the final rating is pulled down to Ba2. For S&P, the indicative rating is also BB with a negative notch for weak GDP per capita around thresholds.

Upgrades in 2026-28E with 2% growth and better fiscal

Consistent real GDP growth of close to 2% over multiple years, along with headline fiscal deficits (<4% of GDP or primary surplus >1% of GDP), could provide a double-notch upgrade in 2026-28. However, we think that moving back to investment grade could require a longer record of stable government, with a GNU set-up beyond 2029, in our view.

Losing investment grade in 2017

South Africa lost its investment grade rating in 2017 at Fitch and S&P, and then in 2020 at Moody’s. A myriad of reasons contributed to this – governance weaknesses, lack of reforms leading to negative per capita growth performance and deteriorating public finances. South Africa fell further into non-investment grade territory in 2020, with foreign currency ratings reaching a bottom of BB- at both Fitch and S&P, and Ba2 at Moody’s in the same year. Moody’s is one notch above the former two. South Africa has been spared further downgrades over the past four years.

Returning to IG still looks unlikely

Returning to investment grade would be a difficult task in the near term. However, rating upgrades may start next year. Our best-case scenario would be two-notch upgrades at Fitch and S&P and one notch at Moody’s within three or four years, taking us to the 2029 election. Another smooth transition in 2029 could strengthen governance and reform momentum, laying the path for a return to investment grade. Moody’s has become more bearish on Africa relative to peers and is less likely to move fast into investment grade.

CPI downside surprises could open room for a cut

In line with our base expectations, SARB paused rate cuts in September with four members in favour of a hold at 7% while two members opted for a25bp cut. We take the view that minority voters indicate that some members think that rate pauses could be at 6.75% rather than the current 7%. In this line of thinking, other committee members could be persuaded to cut one more time should next inflation prints surprise to the downside more significantly.

Our near-term headline inflation projections show an upward trend is on the horizon. We see 3.5% in September, and a jump to 4% in October due to the end of year-on-year fuel deflation. CPI would stay above 4% to year-end. If our baseline holds, no further cuts expected. It’s time to see the effects of previous rate cuts and assess inflation dynamics in coming months. We would reevaluate our rate call should October CPI print less than 4%. For now, we maintain no cuts until 2H 26